2026 DRAM Industry Chain Analysis: Market Trends, Technologies & Global Manufacturers

2026-06-02

As AI model training, cloud computing, and multi-task processing become increasingly central to the digital economy, DRAM has emerged as a critical component defining system performance, computing capacity, and responsiveness. Today, this key memory technology is entering a new super-cycle driven by global demand for artificial intelligence and data infrastructure.

As a volatile memory used for high-speed temporary data processing, DRAM serves as the primary working memory for electronic devices. Together with NAND flash storage, it forms the foundation of the modern digital storage ecosystem and is indispensable for AI computing platforms.

Introduction to DRAM

DRAM, or Dynamic Random-Access Memory, stores data using capacitors that require constant refreshing to maintain charge. It offers extremely fast read and write speeds and ultra-low latency, acting as a vital bridge between the CPU and long-term storage. DRAM is widely deployed across consumer electronics, servers, automotive systems, networking equipment, and security devices to enable efficient and responsive system performance.

1. Core Types of DRAM

DDR (Double Data Rate SDRAM) is the industry-standard memory for desktops, laptops, servers, and data centers. DDR4 and DDR5 are the most common generations today. DDR5 delivers higher bandwidth, improved efficiency, and greater stability, gradually replacing DDR4 as the preferred solution for high-performance computing and data-intensive applications.

LPDDR (Low-Power Double Data Rate) is optimized for mobile and power-sensitive applications. With operating voltages reduced to as low as 0.5V in LPDDR5, it is widely used in smartphones, tablets, automotive electronics, and edge AI devices. LPDDR-based solutions have become essential for smart vehicle systems and portable intelligent devices.

GDDR (Graphics Double Data Rate) memory is purpose-built for GPUs and AI accelerators. GDDR6, GDDR6X, and GDDR7 provide exceptional bandwidth and throughput, making them ideal for graphics rendering, AI model training, and high-performance inference workloads.

HBM (High Bandwidth Memory) uses advanced 3D stacking architecture to achieve unprecedented bandwidth levels. It is a key enabler for AI servers and supercomputers, with terabit-level throughput that addresses critical bottlenecks in large-scale AI model processing.

2. Common DRAM Module Form Factors

UDIMM (Unbuffered Dual Inline Memory Module) is widely used in consumer desktops. It offers low latency, high compatibility, and cost efficiency, making it suitable for daily computing, office work, and entertainment.

SO‑DIMM (Small Outline Dual Inline Memory Module) features a compact form factor designed for laptops, mini PCs, all-in-one systems, and embedded devices where space is limited.

RDIMM (Registered Dual Inline Memory Module) uses registers to improve signal stability and reduce CPU memory controller load. It is the standard choice for enterprise servers, workstations, and data centers.

LRDIMM (Load-Reduced Dual Inline Memory Module) uses advanced buffering to minimize bus load and support extremely high-capacity memory configurations, making it ideal for high-end data centers and AI server platforms.

3. Key Applications

Personal Computing: DRAM determines system responsiveness, multi-tasking performance, software loading speed, and overall user experience.

Mobile Devices: Smartphones and tablets rely on DRAM to enable fast application launches, smooth multitasking, and efficient AI processing.

Servers & Data Centers: Cloud computing, big data analytics, and AI training demand large volumes of high-bandwidth DRAM to support continuous computing workloads.

Networking, Security & Automotive: DRAM supports real-time data processing, intelligent scheduling, and reliable operation in industrial, automotive, and network infrastructure equipment.

Leading DRAM Manufacturers

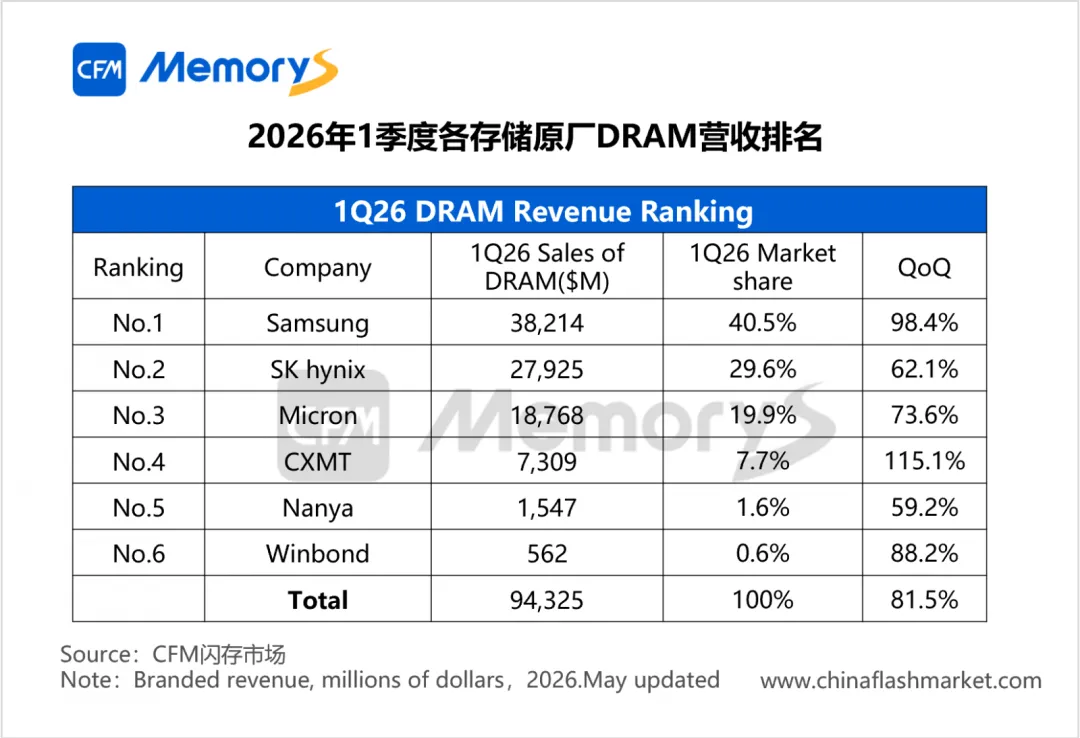

In Q1 2026, the global DRAM market is characterized by a concentrated top-tier structure alongside rapid growth in domestic Chinese suppliers. Leading manufacturers maintain strong advantages in technology, production capacity, and customer relationships, with CXMT as the leading Chinese supplier in the global top five.

Global Major Suppliers

Samsung

Market Share: 40.5% – Global No.1

Quarterly Revenue: $38.21 billion, up 98.4% month-on-month

Strengths: Industry-leading DRAM technology, full DDR5 and HBM product lines, strong presence in both consumer and enterprise markets, high yield and stable performance.

SK hynix

Market Share: 29.6% – Global No.2

Quarterly Revenue: $27.93 billion, up 62.1% month-on-month

Strengths: Global leader in HBM production with over 50% market share, advanced low-power technology, and strong positioning in high-performance AI computing.

Micron

Market Share: 19.9% – Global No.3

Quarterly Revenue: $18.77 billion, up 73.6% month-on-month

Strengths: Mature automotive and industrial-grade DRAM solutions, stable supply chain, balanced product portfolio for server and consumer applications.

Nanya

Market Share: 1.6%

Strengths: Reliable specialty DRAM products for industrial, automotive, and networking applications with strong cost efficiency.

Winbond

Market Share: 0.6%

Strengths: Expertise in small-capacity, high-reliability DRAM for IoT, industrial control, and automotive systems.

Chinese Leading Manufacturer

CXMT

Market Share: 7.7% – Global No.4, with 115.1% month-on-month growth

Quarterly Revenue: $7.31 billion

Strengths: Mass production of self-developed DDR4 and DDR5 DRAM, stable supply, high cost-performance ratio, and a key role in domestic semiconductor substitution.

Major Chinese DRAM Module Brands

GigaDevice, Longsys, Netac, Memblaze, Hongxin Yu, and other domestic manufacturers focus on DRAM module packaging and industry-specific solutions, covering consumer, industrial, and enterprise applications to strengthen the local memory ecosystem.

Q1 2026 DRAM Market Trends

The DRAM industry entered a strong upward cycle in Q1 2026. Surging demand from AI servers, capacity allocation toward HBM, and tight supply of mainstream memory have driven both volume and price increases across the market. Server demand remains the primary growth driver, while consumer electronics markets show steady recovery.

Globally, Samsung, SK hynix, and Micron hold a combined market share of nearly 90%. CXMT continues to gain share with rapid growth, accelerating its presence in mid-to-high-end markets and supporting domestic substitution initiatives.

Technological trends include widespread adoption of DDR5, rapid expansion of HBM, increasing focus on low-power design, and continuous improvements in bandwidth and efficiency. High-performance computing, automotive-grade memory, and industrial storage are expected to drive long-term industry growth, positioning DRAM as a strategic core asset in the AI era.

-

Based in Australia, Silanna Semiconductor leverages extensive expertise in analog chip design and a modular product development platform to deliver a full range of high-speed ADCs. These products cover resolutions from 10 to 16 bits and sampling rates from 20 to 250 MSPS.

-

From July 7 to 9, 2026, Sjoerd Sjoerdsma, Dutch Minister for Foreign Trade and Development Cooperation, led a delegation of 17 Dutch enterprises to China, covering sectors including logistics, agriculture, and high technology. Chip giants such as ASML and NXP were among the most closely watched participants.

-

Multi-layer ceramic capacitors (MLCCs) are very common passive components in various electronic products.

-

Nexperia is a global leading manufacturer of basic semiconductor devices, formerly the Standard Products Division of NXP Semiconductors.

Contact 15/F., Tower B, Regent Centre, 70 Ta Chuen Ping Street, Kwai Chung, N. T,Hong Kong TEL:00852-6763-0779 E-mail:sales@superic.com

SOCIAL

Natural resources