SMCC 2026 Chip Market Analysis: DDR4 Price Surge, Wafer Capacity Shortage

2026-06-17

Overview: Semiconductor Sales Rise for 9 Consecutive Months, Lead Time Extended

The chip industry in 2026 is experiencing an overall supply crunch driven by AI, spreading from memory chips to analog devices and discrete components. Wafer fabs are running at full capacity, inventory of original manufacturers hits bottom, lead time gets longer, and spot prices have doubled or even surged dozens of times.

From January to May 2026, global semiconductor sales reached a recent high, with year-on-year growth rate exceeding 20% for 9 consecutive months. Since May, the average chip lead time has extended to more than 22 weeks, and some products are out of stock.

The supply shortage is prominent in upstream sectors. Huahong Semiconductor has maintained full production for nearly two years. TSMC faces an annual capacity gap of about 20%, and SMIC’s advanced process lines are almost fully loaded. TSMC’s advanced process capacity is fully occupied by AI clients and top manufacturers.

Demand remains strong while capacity expansion lags behind. The chip market will become tighter in the second half of 2026.

Wafer Capacity: Price Hike Becomes Industry Consensus

Wafer foundries across logic chips and memory chips, advanced nodes and mature nodes are preparing for price increases.

TSMC’s sub-7nm advanced capacity is fully taken by AI orders. TI is transitioning from 8-inch to 12-inch wafers, resulting in a lead time of 12-20 weeks. TI will officially raise prices on July 1, and price hikes have been passed down the supply chain.

The packaging & testing sector shows a polarized trend. Leading packaging houses focusing on advanced packaging and memory orders see growing revenue and profits, while small and medium-sized packaging factories face insufficient orders.

DDR4: Structural Shortage to Last for 2-3 Years

DDR4 is the most notable segment in the memory market. Samsung, SK Hynix and Micron have cut their monthly DDR4 capacity by nearly half since 2025, and will phase out DDR4 production lines in 2026 to shift to DDR5 and HBM. By Q4 2026, global DDR4 capacity will drop to 25%-33% of the level in Q1 2025.

DDR4 is facing three major changes: strong demand from industrial control, automotive electronics and communication equipment leads to supply shortage; shrinking production pushes up spot prices; Taiwan-based manufacturers become major suppliers but cannot fill the capacity gap.

The structural shortage of DDR4 will continue for 2 to 3 years. Buyers are advised to build safety inventory in advance.

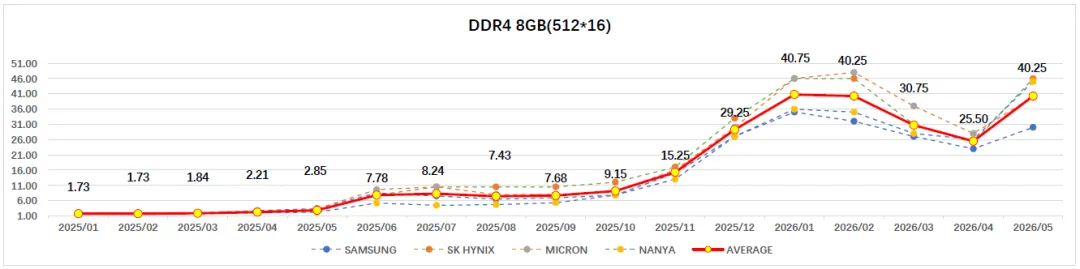

Average Price of DDR4 8Gb 512×16

Jan 2025: $1.73

Jun 2025: $7.78

Dec 2025: $29.25

May 2026: $40.25

The price has increased more than 23 times in over one year, which is extremely rare in semiconductor history.

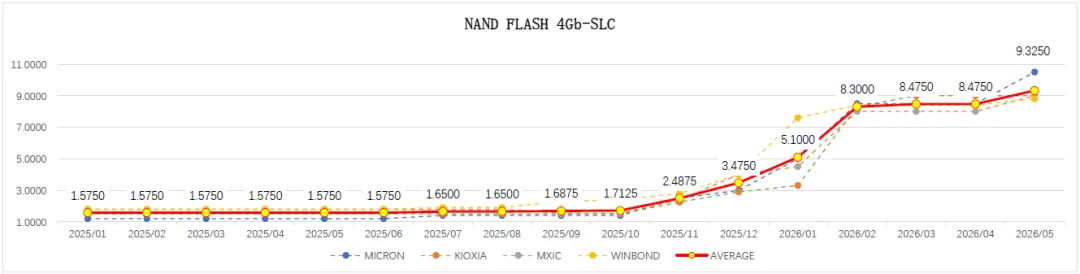

NAND Flash: Price Rises Continuously, SLC Grows Sharply

NAND Flash prices keep rising, especially SLC NAND, driven by strong demand from AI inference and industrial IoT terminals.

Average Price of 1Gb SLC NAND

Jan 2025: $0.60

Jun 2025: $0.63

Dec 2025: $1.90

May 2026: $4.57

Average Price of 4Gb SLC NAND

Jan 2025: $1.58

Jun 2025: $1.58

Dec 2025: $3.48

May 2026: $9.33

Major Brands: Inventory & Price Trend

TI

TI has relatively sufficient inventory currently and will raise prices on July 1. Customers are placing rush orders. The 8-inch to 12-inch wafer transition leads to 12-20 weeks lead time. The price of TMS320F28335 and other DSP products has risen from about $5.6 in 2025 to around $9.5.

ST & ON Semiconductor

The inventory level of ST and ON Semiconductor needs close monitoring. Once inventory falls below the warning line, price hikes and longer lead time will follow.

NXP & Infineon

NXP and Infineon have low inventory and growing orders. Price increases and extended lead time are highly likely.

Discrete Components: Supply-Demand Gap Caused by 8-inch Wafer Shrinkage

Global 8-inch wafer capacity decreased by 2.4% in 2026, while the utilization rate climbed to nearly 90%. MOSFET, IGBT and other discrete components rely heavily on 8-inch mature process, yet most new investments flow into 12-inch and advanced nodes. Many manufacturers are promoting localization and process upgrading to cope with the shortage.

Passive Components: MLCC Demand Surges Driven by AI

AI brings explosive demand for MLCC. MLCC demand for AI servers will grow by 87% in 2026 and another 88% in 2027. A single AI server cabinet consumes 440,000 to 600,000 MLCCs. Inductors also face severe supply shortage.

High-end MLCC market is monopolized by Japanese and Korean enterprises. The capacity expansion cycle lasts 1.5 to 2 years, with limited new capacity in 2026. Raw material costs keep rising, pushing passive component manufacturers to adjust prices.

Inventory Cycle: Lowest Inventory in 3 Years, Downstream Inventory Reduction Completed

The average inventory days of major semiconductor manufacturers dropped to 121 days in Q1 2026, the lowest level in 3 years. The average gross profit margin rose to 74%, showing a booming market with rising volume and price.

Distributors also face tight inventory. Inventory turnover efficiency is improved significantly. Downstream clients have finished destocking, and restocking demand is released.

Three Turning Point Signals for Memory Super Cycle

Signal 1: HBM supply exceeds GPU demand. HBM4 will be mass-produced in late 2026. The supply-demand relationship may reverse from Q4 2026 to Q1 2027 after capacity ramps up.

Signal 2: Real demand decline in consumer memory. 77% of DRAM capacity serves consumer electronics. Sluggish consumer electronics shipments will cause inventory backlog.

Signal 3: Declining investment in AI infrastructure. The sustainability of AI inference demand will determine the long-term trend of memory market.

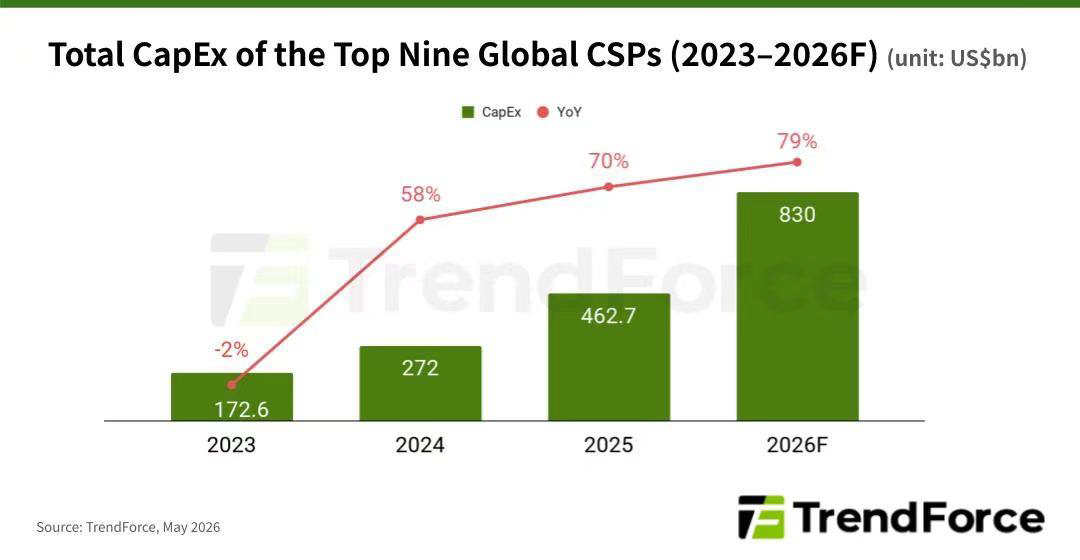

Cloud vendors keep increasing capital expenditure. The total capital expenditure of top 9 cloud providers is revised to 830 billion US dollars in 2026, with annual growth rate adjusted to 79%.

Procurement Strategy Recommendations

Memory products: Sign long-term orders and build 3-6 months safety inventory due to persistent shortage of DDR4 and SLC NAND.

TI analog chips: Complete stock preparation before the price hike on July 1, pay attention to lead time changes caused by wafer transition.

NXP & Infineon: Arrange long-term orders in advance for low inventory and growing orders.

Passive components: Lock up supply for AI-related projects as high-end MLCC capacity is insufficient.

Discrete components: Accept reasonable premium in the short term, and focus on domestic substitution in the long run.

Contact 15/F., Tower B, Regent Centre, 70 Ta Chuen Ping Street, Kwai Chung, N. T,Hong Kong TEL:00852-6763-0779 E-mail:sales@superic.com

SOCIAL

Natural resources