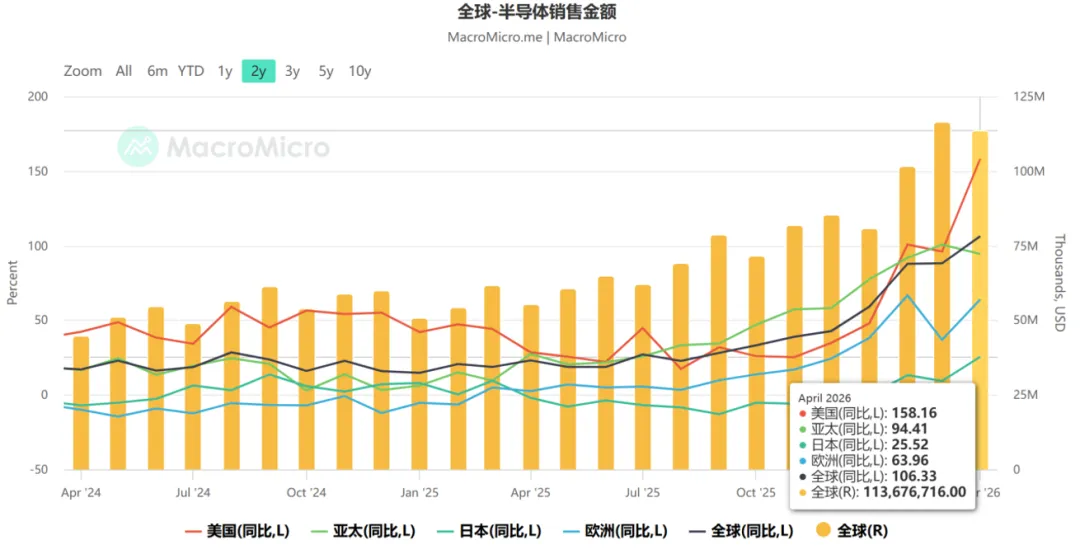

In the first half of 2026, the global semiconductor industry maintains a strong recovery momentum and officially enters a new round of high-boom cycle. As of April 2026, the year-on-year growth rate of global semiconductor sales reached 106.33%, maintaining over 20% growth for 9 consecutive months, and the year-on-year growth rate has doubled in the past year. From upstream wafer manufacturing to downstream distribution terminals, full capacity utilization, inventory de-stocking and price hikes have become the main themes of the industry. However, there are significant structural differentiations among different categories and manufacturers, and supply-demand mismatch is the core logic affecting the annual market trend.

1. Wafer Manufacturing | Capacity utilization surges across the board, and price increases become a common industry consensus

Upstream wafer foundry is the core of this boom cycle. The industry-wide capacity remains in a tight balance, and price hikes have become a common choice for leading manufacturers.

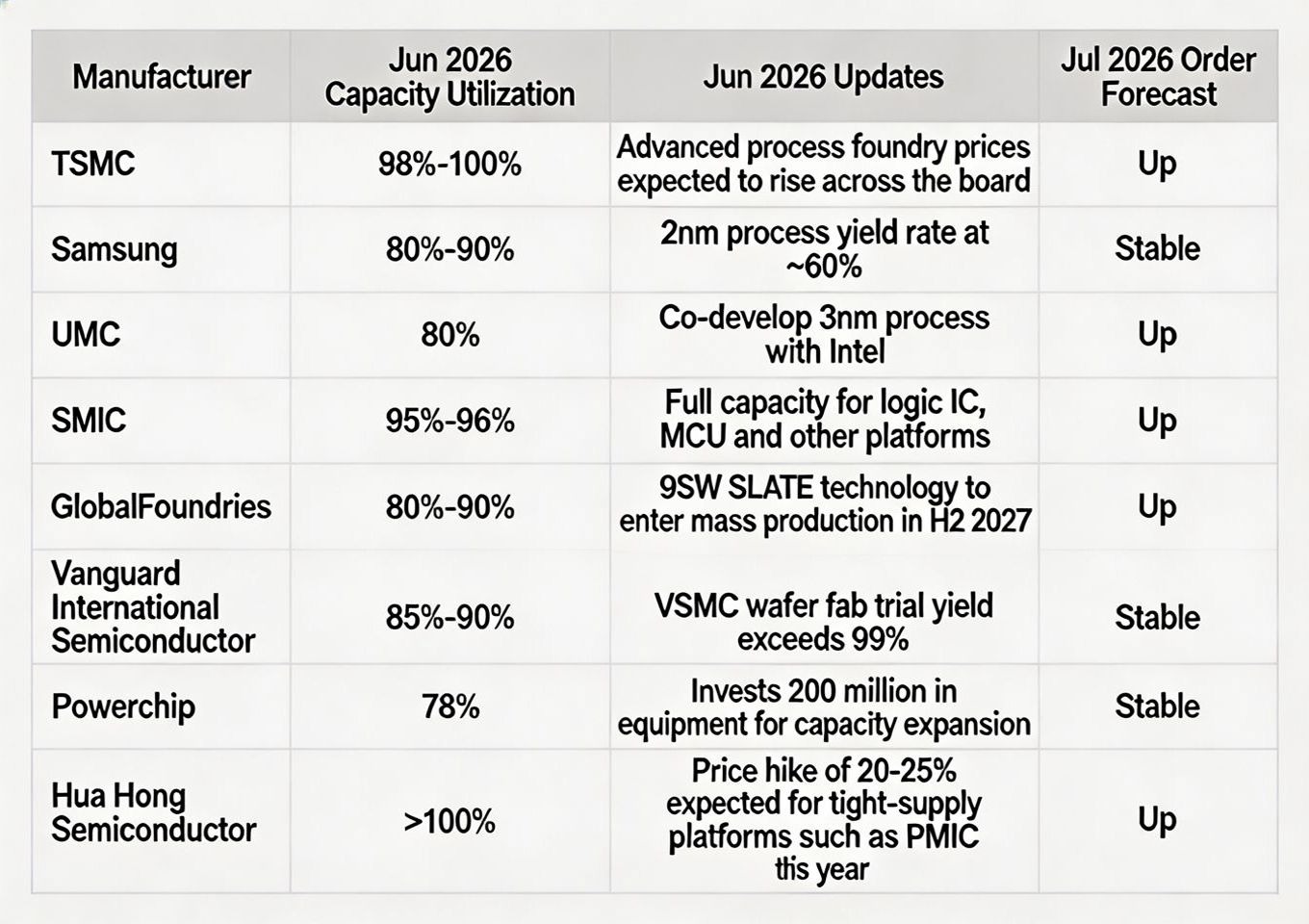

According to the operating data of major wafer fabs in June, leading manufacturers generally maintain high capacity utilization rates:

TSMC's advanced process capacity utilization reaches 98%-100%, and advanced process foundry prices are expected to rise across the board;

SMIC's capacity utilization stands at 95%-96%, with full capacity for logic IC, MCU and other platforms;

Hua Hong Semiconductor's capacity utilization exceeds 100%, and the annual price increase for tight-supply platforms such as PMIC is expected to reach 20%-25%.

Samsung, UMC, GlobalFoundries, Vanguard International Semiconductor and other manufacturers maintain capacity utilization in the range of 80%-90%, and most manufacturers forecast an upward trend in July orders.

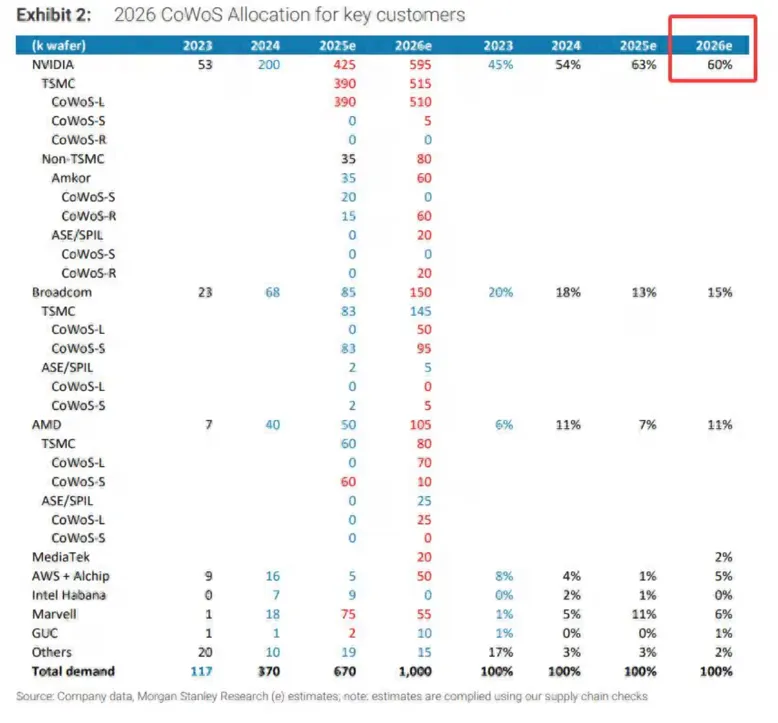

The capacity gap in advanced packaging is even more prominent. TSMC's CoWoS advanced packaging capacity remains tight. Total demand in 2026 is expected to reach 1,000 thousand wafers, of which NVIDIA will consume about 60% of the capacity, followed by tech giants such as AMD, Broadcom and Amazon. The highly concentrated capacity allocation continues to exacerbate the delivery bottleneck of AI computing-related chips.

Notably, a clear "scissors gap" phenomenon has emerged in mature processes: global 8-inch discrete device capacity is expected to decline by 2.4% year-on-year in 2026, while capacity utilization has climbed to a historical high of nearly 90%. The reverse trend of capacity contraction and demand growth has directly pushed up the supply tightness of basic discrete devices.

2. Original Manufacturer Supply-Demand Pattern | Inventories drop to three-year lows, with significant divergence in manufacturer prosperity

With the recovery of downstream demand, global semiconductor original manufacturers have completed deep inventory de-stocking and entered a replenishment cycle. As of the second quarter of 2026, the median inventory turnover days of global semiconductor companies dropped to 118.36 days, 4 days less than the previous quarter, the lowest level in nearly three years; the industry average gross profit margin rose to 84%, and profitability continues to recover.

However, the supply-demand patterns of different tracks and manufacturers are clearly differentiated, which can be divided into three categories:

Tight and rising: NXP and Infineon have low inventories. Increased orders will inevitably lead to price hikes and longer lead times; ONSEMI is facing worsening shortages. Orders from computing and memory manufacturers such as NVIDIA, AMD, Qualcomm, Samsung and SK Hynix are rising simultaneously, with inventories remaining at healthy low levels and the supply-demand gap continuing to widen.

Stable and tightening: Manufacturers such as ST, ADI and Renesas have average inventory levels, with steady growth in orders, and the supply-demand pattern continues to transition to tight balance.

Expectation-driven: TI currently has relatively high inventories, but with the official launch of price hikes in July, it is expected to trigger concentrated downstream orders and quickly consume manufacturer inventories. Meanwhile, TI is promoting the large-scale production line shift from 8-inch to 12-inch wafers, and the lead time for all categories has generally been extended to 12-20 weeks, with strong expectations of supply-side contraction.

In the terminal spot market, price fluctuations have clearly reflected changes in supply and demand: the spot price of TI's TPS54331 power chip rose from 0.73 yuan in mid-2025 to 1.72 yuan in June 2026, an increase of over 135% in one year; the price of STM32F407VET6 microcontroller also shows a volatile upward trend, with significantly intensified price fluctuations in the spot market.

3. Core Market Segments | Memory, passive components and discrete devices rise together, with AI as the core driving force

This boom cycle is not a universal rise. Driven by the three major demand themes of AI computing, automotive electronics and industrial control, the three major segments take the lead in price increases and become the core focus of the market.

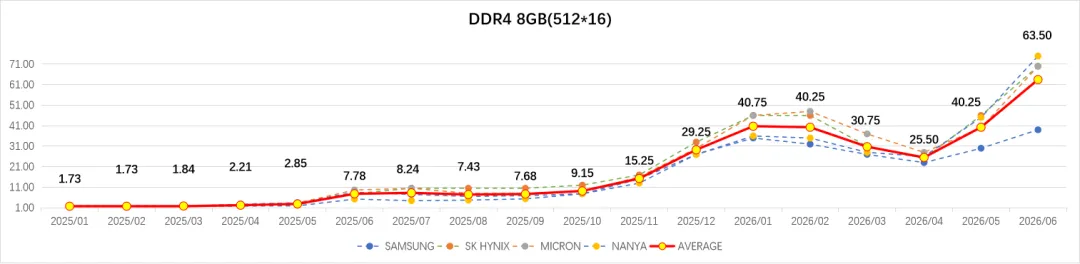

1)Memory: Explosive spot price surge, cycle reversal fully confirmed

The DRAM spot market is witnessing an epic rally. Taking the industry average price as an example, the unit price of mainstream DRAM was only about $1.7 in early 2025, and the industry average price had climbed to $63.5 by June 2026, an increase of over 35 times in a year and a half. Samsung, SK Hynix, Micron and Nanya Technology have raised their quotations simultaneously. The explosive demand from AI servers and data centers is the core driving factor. Coupled with the effect of previous production cuts and inventory de-stocking by manufacturers, the memory industry has fully entered an upward cycle.

2) Passive Components: MLCC prices rise for four consecutive quarters, high-end capacity gap continues to widen

The MLCC industry has entered a continuous price hike cycle. From Q4 2025 to Q2 2026, the quarter-on-quarter growth rates of industry average prices reached 8%, 12% and 10% respectively, and the quarter-on-quarter growth rate is expected to further expand to 18% in Q3 2026.

On the supply side, the high-end MLCC market is highly monopolized by Japanese and Korean manufacturers such as Murata, Samsung Electro-Mechanics and Taiyo Yuden, with a capacity expansion cycle of 1.5-2 years. New high-end capacity in 2026 is extremely limited. Price hikes of upstream dielectric powder and precious metal raw materials such as silver, copper and palladium further push up cost pressure on manufacturers.

On the demand side, AI servers have become the largest source of incremental growth. In 2026, MLCC demand for AI servers will increase by 87% year-on-year, with 440,000 to 600,000 MLCCs used in a single AI cabinet. The supply-demand gap for high-capacity, high-voltage and automotive-grade products continues to widen. In April this year, Murata took the lead in raising prices of high-end models by 15%-40%. In July, Yageo followed suit across its full product line, with consumer-grade specifications rising by 20%-40% and popular AI high-capacity models rising by over 40%.

3) Discrete Devices: 8-inch capacity contraction exacerbates shortages, automotive power devices remain in high demand

The contraction of global 8-inch discrete device capacity has directly pushed up the supply tightness of power devices and small-signal devices. As a global leader in basic semiconductor devices, Nexperia ranks first in the world in market share for small-signal diodes and transistors, ESD protection devices and small-signal MOSFETs, and second in the world for automotive power MOSFETs, serving as a core bellwether for this round of discrete device price hikes.

With the implementation of Nexperia China's independent operation system, the domestic supply chain localization closed loop is accelerating. However, the overall tight supply pattern is difficult to alleviate in the short term. The lead times for automotive-grade and industrial-grade discrete devices continue to lengthen, with obvious spot price premiums.

SMCC has obtained the qualification to place orders directly with Nexperia China official, and has stocked up on some popular models to ensure stable supply for customers.

4. Distribution Channel Signals | Terminal restocking cycle begins, with continuous optimization of inventory turnover

Industry prosperity has fully spread to the distribution industry chain, and the operating data of leading distributors further verify the upward trend of the industry.

In overseas markets, WT's inventory turnover days dropped from 65 days to 50 days; ARROW's inventory turnover ratio increased from 5.0 to 5.9, with significantly accelerated turnover efficiency; AVNET's quarterly inventory amount increased by $185 million, but turnover days still accelerated by 4 days month-on-month. Leading distributors generally take the initiative to optimize inventory structure, spot inventories continue to decline, and stocking strategies to cope with the price hike cycle are more cautious.

The domestic market shows the same trend. The inventory turnover days of local distributors such as CECport, Sunlord Electronics, Liyuan Information, Shannon Semiconductor and Bestar Electronics have declined simultaneously, and AI-related orders have driven significant profit growth. This also marks that the inventory de-stocking of terminal customers is basically over, and a new round of replenishment demand is being released intensively.

5. Second-Half Market Outlook and Supply Chain Response Strategies

Based on the data of the entire industry chain, the high prosperity of the semiconductor industry will continue in the second half of 2026. The three major demand themes of AI computing, automotive electronics and industrial control are clear. Structural shortage under capacity constraints will remain the main tone of the market, and there is still room for price increases of memory, high-end MLCC, automotive power devices and advanced process-related chips.

For downstream terminal enterprises, the mode of relying solely on spot bulk purchases will face the dual risks of price fluctuations and supply disruption. Locking in long-term orders in advance, laying out diversified supply channels, and relying on the market research and source reserve capabilities of professional distributors are the core strategies to cope with this cycle.

As a leading local electronic component distributor, SMCC relies on its global authorized and hybrid distribution network and big data market monitoring system to track real-time changes in prices, inventories and lead times across all categories. We have stocked spot resources of multiple brands including Nexperia, TI, ST, Murata and Samsung, and can provide customers with full-chain supply chain support from market forecasting, stocking planning to technical solutions, helping enterprises control costs and ensure delivery during the price hike cycle.