DDR5 Market Insight: 627% Price Surge, Inter-Generational Price Inversion and Severe Spot Shortages

2026-07-15

DDR5, once a cost-effective and readily available memory solution, has completely rewritten the history of the memory industry cycle. In just one year, DDR5 DRAM chips have surged by an unprecedented 627%, creating a rare inter-generational price inversion where DDR4 now costs more than DDR5. The market has undergone an extreme reversal from "cheap and abundant stock" to "high prices and severe shortages."

Industry-Wide Price Surge

DRAM Chips Skyrocket 627%

The magnitude and duration of this DDR5 price rally have far surpassed both the 2017 DDR4 bull market and the 2021 pandemic-driven surge, setting multiple historical records in the industry.

In the first half of 2025, DDR5 16Gb DRAM chips were priced at just $4.68, a historical low, making bulk procurement highly cost-effective for downstream manufacturers. By October 2025, prices doubled in a single month, and by the end of the year, they had skyrocketed to $34.08, representing a cumulative annual increase of 627%, with a peak monthly surge of over 102%.

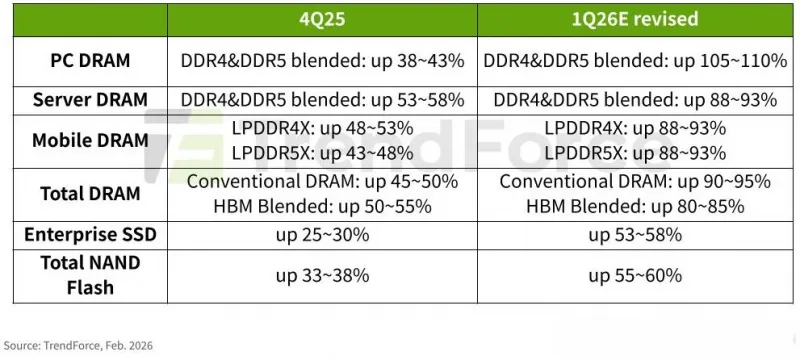

The price wave has rapidly propagated through the entire supply chain. In Q1 2026, contract prices for PC DDR5 surged by 105%–110% month-on-month, while server DDR5 saw an 88%–93% increase.

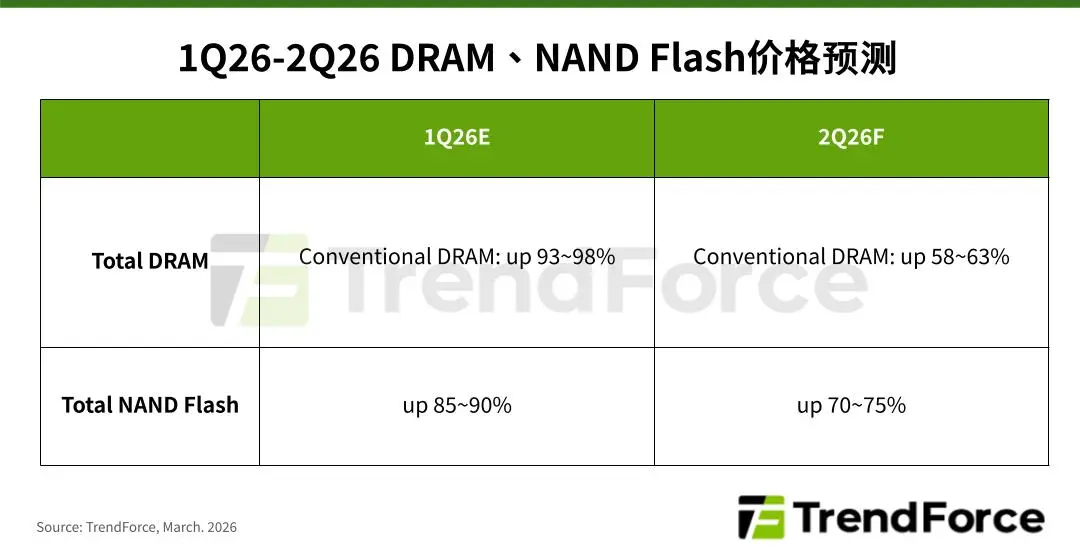

Although Q2 growth moderated slightly, it remained strong at 58%–63% month-on-month. The retail market reflects this volatility even more acutely: mainstream 16GB DDR5 modules have jumped from around $300 to over $1,000. High-frequency, high-density models see daily price adjustments as the norm, and supplier quote validity has been compressed from weeks to just hours, intensifying market tension.

Unprecedented Market Anomaly

DDR4 and DDR5 Price Inversion

According to the traditional memory industry iteration cycle, as the newer DDR5 technology matures and scales, older DDR4 production should contract and prices decline. However, the current market has completely defied this logic—DDR4 spot prices now exceed DDR5, creating a classic inter-generational price inversion.

Guojin Securities' industry chain research confirms that Samsung and SK Hynix have allocated 80%–90% of their advanced DRAM wafer capacity to High Bandwidth Memory (HBM) products. Micron has redirected approximately 70% of its advanced capacity to HBM and high-end server DDR5, systematically squeezing production capacity for consumer-grade and standard DRAM.

SMCC Semiconductor Analysis: The top three memory manufacturers have shifted 70%–80% of their advanced process capacity to HBM and server DDR5. Concurrently, DDR4 production capacity on mature nodes has been reduced, leading to a supply crunch across all memory categories. The traditional safety net of "older, cheaper models" no longer exists. Both new and legacy memory modules face supply shortages and continuous price hikes.

Widening Supply-Demand Gap

"Just-in-Time" Procurement Obsolete

The global DRAM supply-demand deficit reached 4.9% in 2026, with a consumer-grade PC DDR5 shortfall exceeding 10%, the highest level in recent history. Standard order lead times have stretched from 8–12 weeks to over 40 weeks. Major cloud providers and AI computing enterprises have locked in 3–5 year Long-Term Agreements (LTAs), pre-empting massive production capacity and drastically reducing available spot market resources for small and medium-sized manufacturers.

The traditional "order-on-demand, restock-as-needed" procurement model is now obsolete. Many companies face the dilemma of either paying a premium for scarce spot inventory or halting production due to material shortages.

Confronted with this extreme market volatility and structural supply shortage, traditional purchasing strategies are no longer sufficient.

With deep roots in the memory industry, SMCC Semiconductor leverages authoritative market data and a global warehousing network spanning Shenzhen and Hong Kong. We integrate resources from original manufacturers and global distributors to provide end-to-end support, including market trend analysis, global spot allocation, and supply chain security. Our expertise helps clients navigate price cycles and maintain stable production and delivery schedules.

-

DDR5, once a cost-effective and readily available memory solution, has completely rewritten the history of the memory industry cycle. In just one year, DDR5 DRAM chips have surged by an unprecedented 627%, creating a rare inter-generational price inversion where DDR4 now costs more than DDR5. The market has undergone an extreme reversal from "cheap and abundant stock" to "high prices and severe shortages."

-

In the first half of 2026, the global semiconductor industry maintains a strong recovery momentum and officially enters a new round of high-boom cycle.

-

The DDR4 memory chip market is now facing the most severe supply shock in nearly 15 years, and the “older generation costing more than newer” price inversion has evolved from a short-term anomaly into a long-term structural phenomenon.

-

The chip industry in 2026 is experiencing an overall supply crunch driven by AI, spreading from memory chips to analog devices and discrete components.

Contact 15/F., Tower B, Regent Centre, 70 Ta Chuen Ping Street, Kwai Chung, N. T,Hong Kong TEL:00852-6763-0779 E-mail:sales@superic.com

SOCIAL

Natural resources